PPF Interest Rate Guide: Rules, Benifits & Maturity Calculator

Disclaimer: This article is for educational purposes only. It is not financial advice. For personalized guidance, consult a SEBI-registered investment adviser. Bank rates, terms, and tax rules may change – verify key details before taking any action.

Table of Contents

The Public Provident Fund (PPF) is one of India’s most trusted savings schemes. It combines the safety of government backing, attractive long-term returns, and complete tax exemptions. With market volatility and fluctuating FD rates, many savers are asking: What is the latest ppf interest rate and how much can I actually earn after 15 years?

In this Guide, we’ll cover everything about the ppf interest rate, account rules, withdrawal norms, tax benefits, and how to calculate your maturity amount. Whether you invest through SBI, Post Office, or other banks, this guide will help you make the most of your PPF account.

What is PPF?

- PPF full form: Public Provident Fund.

- Launched in 1968 to encourage small savings with assured returns.

- Any Indian resident can open a PPF account at Post Office, SBI, or designated banks.

- Minimum investment: ₹500/year.

- Maximum investment: ₹1.5 lakh/year (tax exemption eligible under Section 80C).

- Lock-in period: 15 years, extendable in 5-year blocks.

- You can invest lump sum or in installments (up to 12 installments in a year).

A PPF account online can now be opened via SBI, ICICI, HDFC, and other net banking platforms. Returns from PPF will be same for all banking platforms. Considering your salaried bank would be easier to you to manage all at one place.

PPF Interest Rate 2025 & Historical Trends

The ppf interest rate 2025 is 7.10% per annum (compounded annually), applicable for FY 2025-26. This rate is notified every quarter by the Ministry of Finance.

How Interest is Calculated

- Interest is computed on the lowest balance between the 5th and last day of each month.

- Deposits made before the 5th of the month earn interest for that month.

- Interest is credited annually on March 31st.

Recent Interest Rate History

| Financial Year | PPF Interest Rate |

|---|---|

| 2025-26 | 7.10% |

| 2024-25 | 7.10% |

| 2023-24 | 7.10% |

| 2022-23 | 7.10% |

| 2020-21 | 7.10% |

Stable rates mean predictable growth, which makes PPF attractive compared to bank deposits.

PPF Calculator – Estimate Your Returns

A PPF calculator helps you project how much corpus you’ll build over time. You can also use SBI PPF calculator or Post Office PPF calculator, but most tools show only corpus, not the split between principal and interest.

Example 1: Max Contribution (₹1.5 lakh annually)

- Principal invested: ₹22,50,000

- Interest earned: ~₹15,56,239

- Total corpus: ~₹37,06,239

Example 2: Small Saver (₹10,000 annually)

- Principal invested: ₹1,50,000

- Interest earned: ~₹1,03,748

- Total corpus: ~₹2,53,748

Try our interactive PPF calculator to compare contributions, tenure, and expected returns.

Tax Benefits of PPF (EEE Advantage)

PPF offers a triple tax advantage (EEE status):

- Exempt Investment – Up to ₹1.5 lakh deductible under Section 80C.

- Exempt Interest – Entire interest earned is tax-free.

- Exempt Maturity – Final maturity amount is 100% tax-free.

This makes PPF one of the most tax-efficient investments compared to FDs or debt funds.

PPF Withdrawal Rules & Lock-In Period

- Lock-in period: 15 years.

- Partial withdrawals: Allowed from the 7th financial year. You can withdraw up to 50% of the balance at the end of the 4th year or previous year, whichever is lower.

- Premature closure: Allowed after 5 years for education or medical treatment, with 1% interest penalty.

- Loan facility: Available from 3rd to 6th year (up to 25% of balance).

- Missed deposits: If you don’t invest for a year, account becomes inactive but can be revived with a small penalty.

PPF withdrawal rules are stricter than bank FDs but ensure long-term discipline.

Regularization of Irregular PPF Account – My Experience

I had opened my PPF account with SBI back in 2018 with an initial deposit of ₹2,000. However, I stopped investing after that and my account turned inactive. In September 2025, I decided to reactivate it. To regularize, I paid a penalty of ₹350 along with ₹3,500 (₹500 for each of the 7 missed years) through online net banking facility. My PPF account was then successfully restored to active status.

This was completely online process. If you have net banking facility, it’s a matter of 2 minutes.

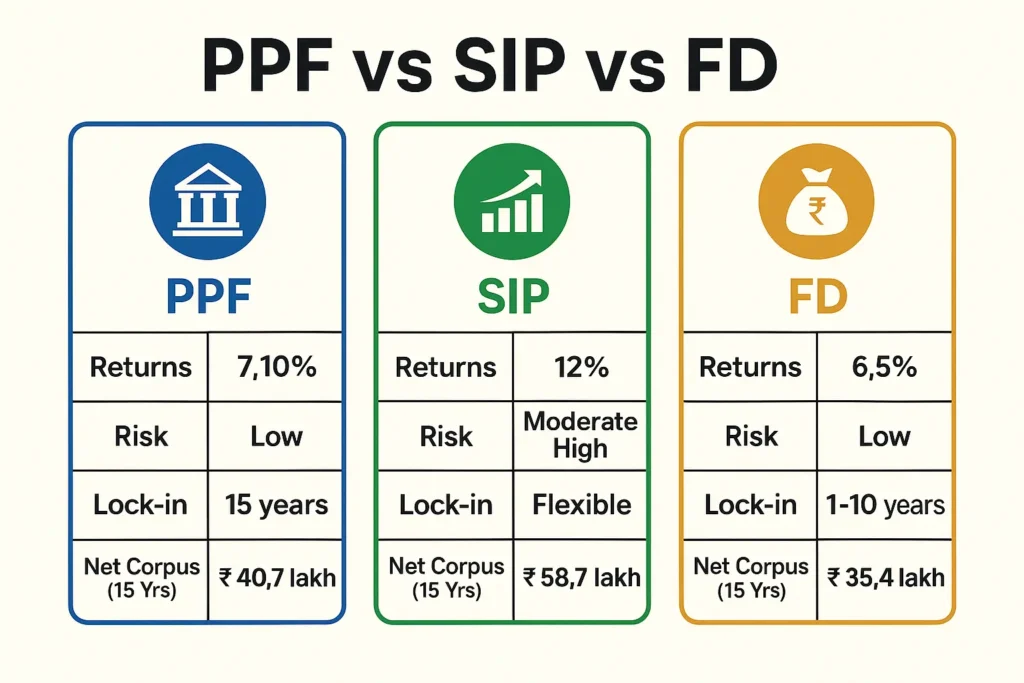

PPF vs SIP vs FD – Which is Better?

| Feature | PPF (Public Provident Fund) | SIP (Equity Mutual Fund @12%) | Fixed Deposit (6.5%) |

|---|---|---|---|

| Principal Invested (15 yrs) | ₹22,50,000 | ₹22,50,000 | ₹22,50,000 |

| Gross Corpus After 15 Yrs | ₹40,68,209 | ₹62,62,992 | ₹38,63,102 |

| Interest / Returns Earned | ₹18,18,209 | ₹40,12,992 | ₹16,13,102 |

| Tax Treatment | EEE (No Tax) | LTCG: 10% on gains above ₹1 lakh | 20–30% tax on full interest |

| Net Corpus After Tax | ₹40,68,209 | ~₹58,71,692 | ~₹35,40,481 |

| Risk Level | Very Low (Govt-backed) | Moderate–High (market-linked) | Low |

| Lock-in Period | 15 years (extendable) | Flexible (no lock-in for open-ended funds; ELSS 3 years) | 1–10 years |

| Best For | Safe, tax-free, long-term savings | Higher growth & wealth creation | Short-term guaranteed savings |

Note:

- PPF Interest Rate 2025 (7.10%) gives a safe and tax-free corpus of ~₹40.7 lakh in 15 years.

- SIP in Equity Mutual Funds (12% CAGR) can grow to ~₹62.6 lakh before tax, ~₹58.7 lakh after LTCG. If you are considering to do SIP you can explore one more Tax Savings Investment Scheme called Equity Linked Savings Scheme ELSS.

- FDs at 6.5% give ~₹38.6 lakh before tax, ~₹35.4 lakh after tax (assuming 20% tax slab).

The ppf interest rate of 7.10% in 2025 makes PPF a stable, tax-efficient, and safe investment option. With its 15-year lock-in, it’s best suited for long-term goals like children’s education or retirement. While it may not beat equity returns, it remains unmatched in security + tax savings.

Manage your PPF account:

- Deposit before the 5th of each month,

- Stay consistent for 15 years,

- Use a PPF calculator to project your corpus.

PPF is not just a savings account—it’s a disciplined wealth-builder backed by the Government of India.

Frequently Asked Questions (FAQs)

How much will I get after 15 years in PPF?

If you invest ₹1.5 lakh annually at the current ppf interest rate of 7.10%, you’ll get around ₹37 lakh after 15 years.

What does PPF stand for?

PPF stands for Public Provident Fund, a government-backed savings scheme.

What is PPF and its benefits?

It’s a long-term savings scheme with guaranteed returns, tax exemption, and 15-year lock-in. Benefits include safety, tax-free returns, and loans/withdrawals after certain years.

Is PPF giving 12% returns?

No, the current rate is 7.10%. Historically, it has ranged between 7–12%, but it hasn’t touched 12% for many years.

How long is the PPF lock-in period?

15 years, extendable in 5-year blocks.

Is PPF better or SIP?

PPF is safer with fixed returns; SIP offers potentially higher but market-linked returns.

Can I withdraw my PPF after 2 years?

No, partial withdrawals are allowed only after the 7th financial year.

What happens if I don’t pay PPF for 1 year?

Your account becomes inactive but can be revived by paying a ₹50 penalty per missed year plus the minimum ₹500 deposit.

Is PPF tax-free?

Yes, contributions, interest, and maturity are all tax-free under Section 80C.

Is it necessary to put money in PPF every year?

Yes, at least ₹500 must be deposited each year to keep the account active.