NPS/UPS Pension Scheme Latest Update

Table of Contents

The Government of India has recently approved the extension of new investment options — Life Cycle 75 (LC75) and Balanced Life Cycle (BLC) — to Central Government employees under both the NPS and the UPS scheme.

The UPS Pension Scheme is crucial for government employees to secure their retirement. Understanding the specifics of the UPS Pension Scheme can help maximize benefits.

What is the UPS Pension Scheme?

With the UPS Pension Scheme, subscribers can expect tailored investment strategies that align with their retirement goals.

The UPS pension scheme is a government-designed retirement investment framework under which government employees contribute and accumulate corpus through defined contributions. Under UPS (and NPS similarly), subscribers benefit from market-linked growth, tax advantages and structured withdrawal/annuity features at retirement.

What’s new?

- Central Government employees can now choose from additional Auto-Choice / Life Cycle fund options, including LC75 and BLC, providing higher equity exposure and longer equity run-up period.

- For LC75, the maximum equity allocation is now up to 75%, tapering gradually from age 35 to 55.

- Under BLC, equity allocation remains higher until age 45 before tapering, enabling longer equity participation.

- These changes bring greater flexibility, allowing employees to align retirement corpus growth with their risk-return preferences.

| Age | LC75 | LC50 | Balanced LC50 | LC25 |

|---|---|---|---|---|

| Up to 35 Years | E: 75%, C: 10%, G: 15% | E: 50%, C: 30%, G: 20% | E: 50%, C: 30%, G: 20% | E: 25%, C: 45%, G: 30% |

| 36 Years | E: 71%, C: 11%, G: 18% | E: 48%, C: 29%, G: 23% | E: 50%, C: 30%, G: 20% | E: 24%, C: 43%, G: 33% |

| 37 Years | E: 67%, C: 12%, G: 21% | E: 46%, C: 28%, G: 26% | E: 50%, C: 30%, G: 20% | E: 23%, C: 41%, G: 36% |

| 38 Years | E: 63%, C: 13%, G: 24% | E: 44%, C: 27%, G: 29% | E: 50%, C: 30%, G: 20% | E: 22%, C: 39%, G: 39% |

| 39 Years | E: 59%, C: 14%, G: 27% | E: 42%, C: 26%, G: 32% | E: 50%, C: 30%, G: 20% | E: 21%, C: 37%, G: 42% |

| 40 Years | E: 55%, C: 15%, G: 30% | E: 40%, C: 25%, G: 35% | E: 50%, C: 30%, G: 20% | E: 20%, C: 35%, G: 45% |

| 41 Years | E: 51%, C: 16%, G: 33% | E: 38%, C: 24%, G: 38% | E: 50%, C: 30%, G: 20% | E: 19%, C: 33%, G: 48% |

| 42 Years | E: 47%, C: 17%, G: 36% | E: 36%, C: 23%, G: 41% | E: 50%, C: 30%, G: 20% | E: 18%, C: 31%, G: 51% |

| 43 Years | E: 43%, C: 18%, G: 39% | E: 34%, C: 22%, G: 44% | E: 50%, C: 30%, G: 20% | E: 17%, C: 29%, G: 54% |

| 44 Years | E: 39%, C: 19%, G: 42% | E: 32%, C: 21%, G: 47% | E: 50%, C: 30%, G: 20% | E: 16%, C: 27%, G: 57% |

| 45 Years | E: 35%, C: 20%, G: 45% | E: 30%, C: 20%, G: 50% | E: 50%, C: 30%, G: 20% | E: 15%, C: 25%, G: 60% |

| 46 Years | E: 32%, C: 20%, G: 48% | E: 28%, C: 19%, G: 53% | E: 48%, C: 28%, G: 24% | E: 14%, C: 23%, G: 63% |

| 47 Years | E: 29%, C: 20%, G: 51% | E: 26%, C: 18%, G: 56% | E: 46%, C: 26%, G: 28% | E: 13%, C: 21%, G: 66% |

| 48 Years | E: 26%, C: 20%, G: 54% | E: 24%, C: 17%, G: 59% | E: 44%, C: 24%, G: 32% | E: 12%, C: 19%, G: 69% |

| 49 Years | E: 23%, C: 20%, G: 57% | E: 22%, C: 16%, G: 62% | E: 42%, C: 22%, G: 36% | E: 11%, C: 17%, G: 72% |

| 50 Years | E: 20%, C: 20%, G: 60% | E: 20%, C: 15%, G: 65% | E: 40%, C: 20%, G: 40% | E: 10%, C: 15%, G: 75% |

| 51 Years | E: 19%, C: 18%, G: 63% | E: 18%, C: 14%, G: 68% | E: 39%, C: 18%, G: 43% | E: 9%, C: 13%, G: 78% |

| 52 Years | E: 18%, C: 16%, G: 66% | E: 16%, C: 13%, G: 71% | E: 38%, C: 16%, G: 46% | E: 8%, C: 11%, G: 81% |

| 53 Years | E: 17%, C: 14%, G: 69% | E: 14%, C: 12%, G: 74% | E: 37%, C: 14%, G: 49% | E: 7%, C: 9%, G: 84% |

| 54 Years | E: 16%, C: 12%, G: 72% | E: 12%, C: 11%, G: 77% | E: 36%, C: 12%, G: 52% | E: 6%, C: 7%, G: 87% |

| 55 Years | E: 15%, C: 10%, G: 75% | E: 10%, C: 10%, G: 80% | E: 35%, C: 10%, G: 55% | E: 5%, C: 5%, G: 90% |

Why this matters

Adapting to changes within the UPS Pension Scheme can enhance your retirement savings.

- Flexibility: Government employees now have a broader range of options similar to non-government subscribers.

- Risk optimisation: The “glide-path” mechanism ensures equity allocation reduces as retirement nears, protecting against market volatility.

- Better growth potential: Higher equity share means more opportunity for growth over long horizons.

- Tailored planning: Individuals can now pick a corpus path that matches their age, risk appetite and retirement timeline.

How to Change Corpus Allocation under the UPS / NPS Scheme

Whether you are a government subscriber under UPS, NPS for private sector employees, or self-employed participant, here’s a step-by-step guide to changing your investment option or switching life-cycle fund.

Step 1: Verify your subscriber category

- Central Government employees under the UPS/NPS scheme.

- State government / public sector employees under state-adopted NPS/UPS.

- Private sector / corporate subscribers under NPS.

Each category follows similar technical steps though some portals may differ.

Step 2: Log in to Subscriber Interface

Each aspect of the UPS Pension Scheme is designed to cater to the unique needs of government employees.

Ensuring you are informed about the UPS Pension Scheme is vital for effective retirement planning.

- Visit the official portal of the Pension Fund Regulatory and Development Authority (PFRDA) — for NPS/UPS.

- Use your credentials (PRAN, password, OTP) to login to the NPS subscriber e-Service portal.

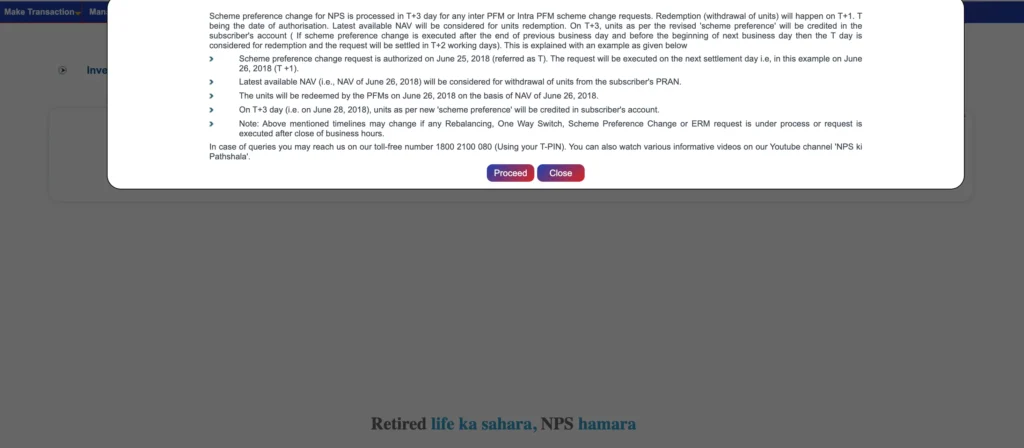

Step 3: Navigate to Change PFM Asset Class

- Once you click on “Change PFM-Asset Class” you are redirected to select which tier you want to select.

- Select which tier you want to change the Asset Class whether it is tier 1, tier 2 etc.

- After submitting your desired asset class a pop up instructions will appear as shown below. Click Proceed.

Step 4: Initiate Investment Choice Request

Utilizing the benefits of the UPS Pension Scheme requires careful consideration of each investment choice.

- After you click on proceed, you will be redirected to Investment Choice Request window. Here you can check your existing investment choice and a submit button to initiate New Investment Scheme Choice as shown below.

Step 5: Submit the Request

- In the New Investment Scheme Choice you can select your desired new allocation.

- Click on submit.

- Once you click on submit button you will get a mobile OTP. Submit OTP and your request will be initiated.

How to select your desired new allocation

- Selecting your desired new allocation is very simple.

- Analyse your risk appetite, If you are a risk taker and have stock market knowledge then choose higher Life Cycle (LC 75) or other wise choose lower Life Cycle (LC 50 or LC 25).

Points to Note

- Some states or employer-administered schemes might require offline form submission through HR/pension cell.

- Always read the ‘Terms & Conditions’ of switching — in some cases, funds might apply from next contribution cycle.

- Higher equity exposure = higher risk and higher potential return — ensure it matches your age and retirement timeline.

Who Can Benefit from the UPS Pension Scheme Update?

Central Government Employees

If you are a central government employee under UPS/NPS, this update gives you new avenues to optimise your retirement corpus.

State Government & Public Sector Employees

Though the announcement is specifically for central employees, many states may adopt similar options. Keep an eye on your state’s notifications.

Private Sector Subscribers

While UPS is government-employee specific, private sector employees under NPS can also use similar life-cycle options — although LC75/BLC extension may vary by scheme.

Self-Employed & Individual NPS Subscribers

You can choose your own investment option in NPS (Active choice or Auto choice) and benefit from similar life-cycle designs; consult your fund manager or broker if you wish to switch.

Impact on Retirement Planning & Portfolio Strategy

- A higher equity share (like LC75) suits younger employees (age 20–35) who can ride market volatility and aim for higher corpus.

- As you age, the tapering automatically reduces equity and increases safer assets — aligning with retirement protection.

- For employees close to retirement, low-risk options like Scheme G (100% Government Securities) may make more sense.

- This change encourages active planning rather than “set and forget” — you now have to make an informed choice.

- Consider other retirement pillars (PPF, EPF, annuities) along with UPS/NPS to build a diversified retirement corpus.

Know about more investment opportunities like NPS Vatsalya Scheme

Frequently Asked Questions (FAQ)

Can I switch from LC-50 to LC-75 under UPS?

Yes — central government employees can opt for LC-75 or BLC under the new rule. If you were under LC-50, you can switch subject to your scheme’s guidelines.

Is switching online free?

Generally yes — submitting via the web portal is free, though your employer or state scheme may have internal admin fees.

Will my future contributions automatically follow the new allocation?

Once the switch is accepted, yes – future contributions will follow the selected option. Monitor your account to confirm.

What happens if I stay in the default option?

If you do not switch, your corpus will continue in the default investment pattern defined by PFRDA or your employer.

The extension of LC75 and BLC into the UPS pension scheme marks a significant step in offering choice, flexibility and modern investment design for government employees. If you’re part of UPS or NPS, evaluate your age, risk appetite and retirement timeline — then make a thoughtful choice. Do not ignore this update: review your corpus allocation, log in to your portal and make the switch if it fits your strategy. After all, retirement planning is a marathon — the earlier you optimise, the stronger your finish line will be.

Source: PIB

Transitioning to the UPS Pension Scheme allows for better planning and security in retirement.

Active management of your UPS Pension Scheme can enhance your financial outcomes.

Choosing the right path within the UPS Pension Scheme will lead to a more secure future.

Evaluate your options within the UPS Pension Scheme regularly for optimal growth.

Embrace the benefits of the UPS Pension Scheme to secure your retirement effectively.

Finally, understanding and leveraging the UPS Pension Scheme will ensure a stronger retirement.