NPS Vatsalya Scheme: Complete Guide

The NPS Vatsalya Scheme regulated by PFRDA is a special pension plan launched by the Government of India to help parents/guardians secure the financial future of their minor children. Under this scheme, contributions begin when a child is a minor, and the account converts into a regular NPS account once the child turns 18. If you’re wondering how NPS Vatsalya works, what its benefits are, or how much corpus you can build using the NPS Vatsalya calculator, this guide will walk you through everything in simple terms.

1. What is NPS Vatsalya Scheme?

NPS Vatsalya is a subset of the National Pension System (NPS), regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It is exclusively for minors (Indian citizens under age 18). Account is opened by a guardian or parent. Minimum contribution is ₹1,000 per annum; there is no upper limit. This makes it accessible to many.

2. Key Features & Benefits of NPS Vatsalya Scheme

- The scheme encourages early savings and compounding since contributions begin when the child is young.

- Flexibility: Contributions can be annual or monthly, and parents/guardians can pick the investment mixture (for example, a “Moderate” lifecycle fund mix) under Auto, Moderate, or Active choice.

- Like PPF and ELSS, the NPS Vatsalya Scheme also provides tax deductions that parents can claim.

- Tax benefits: Contributions to NPS Vatsalya are eligible under Section 80CCD(1B), which allows an additional deduction (up to ₹50,000) besides Section 80C.

3. Withdrawal Rules & What Happens When Child Turns 18

- Partial withdrawals: Allowed after 3 years of account opening. Withdrawals up to 25% of contribution for specific reasons like education, medical illness, or disability. Maximum three times until child becomes major.

- On attaining age 18, the account is automatically converted to a regular NPS Tier-I account. Fresh KYC must be done.

- Exit rules: If the corpus is more than ₹2.5 lakh, 80% must be used to purchase an annuity, 20% can be withdrawn. If less or equal to ₹2.5 lakh, full corpus can be withdrawn as lump sum.

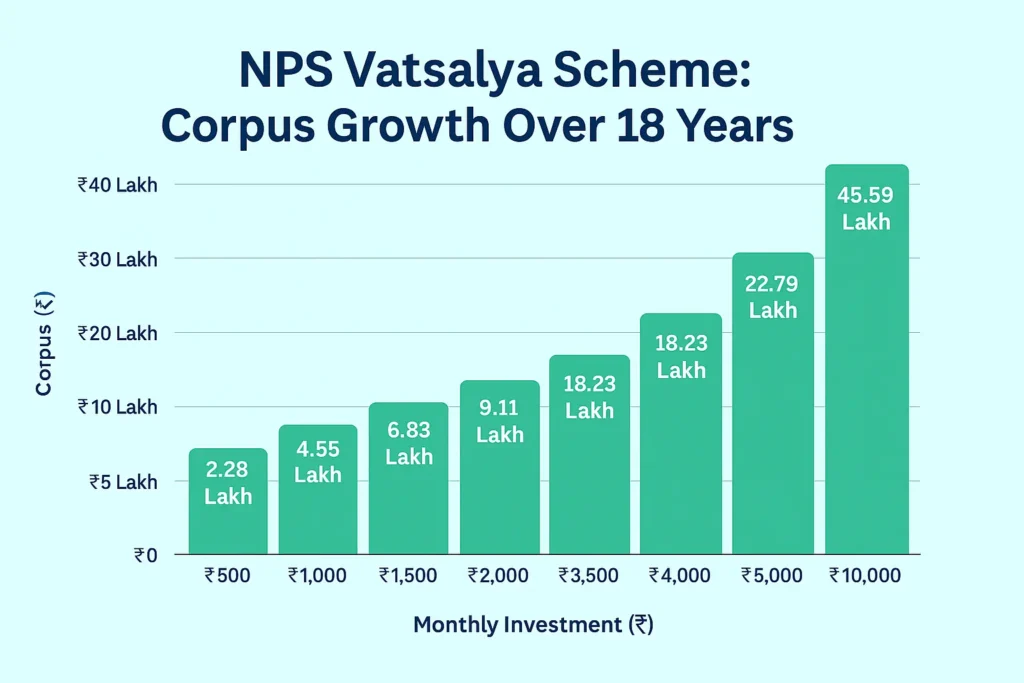

How much return in NPS vatsalya scheme?

Here I have estimated and created how much return you can earn over 18 years. I hope this will give you a clear picture of corpus growth in NPS Vatsalya scheme. Plan accordingly to gift your child after 18 years.

4. How to Use the NPS Vatsalya Calculator & What It Shows

- The NPS Vatsalya calculator (for example on PensionBox or official portals) allows you to input your child’s age, expected contributions (monthly/annual), rate of return, and project corpus at age 18 or beyond.

- Example: If you invest ₹10,000 annually under NPS Vatsalya with ~10% rate of return for 18 years, the corpus might become ~₹5 lakh by age 18; if continued until retirement, possibly crores depending on return and compounding.

5. Eligibility & Who Should Consider NPS Vatsalya

Eligibility: Indian minors, including NRIs/OCIs minors, with guardians opening on their behalf. Parents who want early financial discipline and a long-term savings pool for their child’s future (education, beyond) should strongly consider this scheme.

6. Pros & Cons of NPS Vatsalya Scheme

Pros:

- Low minimum contribution (₹1,000 p.a.) makes it accessible.

- Long time horizon → powerful compounding.

- Tax savings under Section 80CCD(1B).

- Automatic transition to NPS Tier-I when child turns 18.

Cons:

- Partial withdrawals allowed only under limited conditions and only after 3 years.

- Returns are market linked → risk of variation.

- Annuity purchase at retirement might reduce lump sum benefit.

- Costs / CRA maintenance charges may apply. (Recent PFRDA update revised CRA charges for NPS, NPS Vatsalya accounts effective from October 2025)

7. Frequently Asked Questions (FAQs)

What is the NPS Vatsalya Scheme?

The NPS Vatsalya Scheme is a special pension product under the National Pension System (NPS) designed for minors. Parents or guardians can open the account on behalf of a child below 18 years. Contributions start early, enjoy tax benefits, and the account automatically converts into a regular NPS Tier-I account when the child turns 18.

Is it good to invest in the NPS Vatsalya Scheme?

Yes, the NPS Vatsalya Scheme is a good choice if you want to secure your child’s financial future with long-term compounding and tax deductions under Section 80CCD(1B). However, since returns are market-linked, it is better suited for parents who can stay invested for 15–20 years or more and want retirement-style security for their children.

What happens to NPS Vatsalya after 18 years?

When the child turns 18, the NPS Vatsalya account automatically converts into a regular NPS Tier-I account. At that point, the child must complete KYC with their own documents and can continue contributing like any other NPS subscriber. If the corpus is above ₹2.5 lakh, 80% must be used to buy an annuity, and 20% can be withdrawn.

Which is better, NPS Vatsalya or PPF?

NPS Vatsalya: Market-linked returns (around 9–10% historically), long-term compounding, tax benefits, but subject to some withdrawal restrictions.

PPF: Fixed 7.10% interest rate, 15-year lock-in, fully tax-free maturity, government-backed safety.

👉 If you prefer guaranteed tax-free returns, choose PPF. If you want higher growth potential with some risk, NPS Vatsalya may be better.Which is better, NPS Vatsalya or Sukanya Samriddhi Yojana?

NPS Vatsalya: Available for both boys and girls, market-linked growth, converts to NPS Tier-I at 18.

Sukanya Samriddhi Yojana (SSY): Exclusively for girls, fixed interest (currently 8.2%), lock-in till 21 years, tax-free maturity.

👉 If your child is a girl, SSY gives higher guaranteed returns than PPF and is risk-free. For both boys and girls, NPS Vatsalya offers equity-linked growth and retirement-style planning.Is NPS Vatsalya tax-free?

Contributions to the NPS Vatsalya Scheme qualify for tax deductions under Section 80C (up to ₹1.5 lakh) and an additional Section 80CCD(1B) deduction of ₹50,000. However, at maturity, the annuity portion purchased may be taxable as per income slab, while the lump sum withdrawal is tax-free.

Is NPS Vatsalya only for girls?

No, unlike Sukanya Samriddhi Yojana, the NPS Vatsalya Scheme is open for all minor children (both boys and girls). Any Indian citizen under 18 years of age can have an account opened on their behalf by a parent or guardian.

How to join NPS Vatsalya?

You can join the NPS Vatsalya Scheme by visiting authorized banks (like SBI, ICICI, HDFC, PNB) or Post Offices that provide NPS services. Submit the child’s birth certificate, guardian’s KYC documents, and the minimum contribution (₹1,000). After account opening, contributions can be made online or offline until the child turns 18.

The NPS Vatsalya Scheme offers an excellent opportunity for parents/guardians to begin retirement/future savings for minors with small contributions, tax benefits, and long-term growth potential. If you’re thinking about securing your child’s financial future, start early, use the NPS Vatsalya calculator to estimate how much you need to invest, and choose a fund mix that balances growth and risk.