Unified Pension Scheme 2025: Hidden Rules You Must Know

The Central Government has introduced a Unified Pension Scheme (UPS) under the National Pension System (NPS), bringing significant changes for government employees. These new rules, effective April 1, 2025, aim to provide better financial security post-retirement. Before going to know all hidden rules you must know, let’s take an overview of the Unified Pension Scheme.

Overview of the Unified Pension Scheme

1. What is the Unified Pension Scheme (UPS)?

The Unified Pension Scheme (UPS) is a newly introduced pension scheme under the NPS framework. It is designed for central government employees, offering an assured pension along with benefits like family pension, lump-sum payouts, and structured withdrawals.

2. Who is Eligible for the New Pension Scheme?

Employees eligible for UPS include:

- Existing central government employees who are part of NPS as of April 1, 2025.

- New recruits joining government service on or after April 1, 2025.

- Retired employees under NPS who were part of NPS but opted for voluntary retirement before the implementation of UPS.

- Spouse in case of a subscriber who has superannuated or retired and has demised before exercising the option for UPS.

3. Key Features of the New Pension Rules

A. Guaranteed Pension

Unlike NPS, which depends on market-linked returns, UPS ensures a fixed monthly pension after retirement, providing financial stability.

B. Government Contribution

- An employee contributes 10% of basic pay + dearness allowance (DA).

- The government contributes equal to 10% of the employee’s salary.

C. Minimum Guaranteed Pension

- Employees completing at least 10 years of service will receive a minimum guaranteed pension of ₹10,000 per month.

- The pension amount depends on salary and total years of service.

- Use our UPS Pension calculator to understand better.

D. Lump-Sum Payment at Retirement

- Employees will receive one-time lump-sum benefits at the time of retirement.

- The amount will be calculated based on the final salary and completed years of service.

E. Family Pension & Survivor Benefits

- In case of the employee’s death, the legal spouse will continue receiving 60% of the pension amount.

- Additional benefits include death gratuity and financial aid for dependents.

4. How do you switch from NPS to UPS?

Employees under NPS can opt into UPS within 3 months of the scheme’s implementation. The government has provided a one-time option for employees to migrate from NPS to UPS by submitting an official application. Once you opt for UPS you cannot go back to NPS again.

5. NPS vs UPS

| Feature | National Pension System (NPS) | Unified Pension Scheme (UPS) |

|---|---|---|

| Pension Guarantee | Market-linked, no guarantee | Fixed monthly pension |

| Government Contribution | 14% of basic salary | Not Defined |

| Withdrawal | Limited withdrawal | Lump-sum payment at retirement |

| Family Pension | Not available | 60% pension to spouse |

| Minimum Pension | Not defined | ₹10,000/month |

The Unified Pension Scheme (UPS) 2025 is a significant step toward providing government employees with a secure retirement. It offers a guaranteed pension, family benefits, and better financial stability compared to the traditional NPS. If you’re a government employee, you must decide quickly whether to opt-in to UPS before the deadline.

But Wait, Now I will discuss the hidden rules with you. So, that you get more awareness to opt-int to UPS or not.

Key Points You Must Know Before Decide to go UPS

1. Understanding Pool Corpus:

pool corpus shall comprise of:

- If your Basic Pay + Dearness Allowance (DA) is ₹60,000. Then Individual corpus will be 10% of Basic and DA by you and your employer, that is ₹12,000 (6000+6000).

- Pooled Corpus will be 8.5% of your basic pay and DA, which is ₹5,100 and is contributed by the government. Unused individual corpus from employees who exit early (Regulation 19(3)) is also added to the Pooled Corpus.

- The objective is to provide a regular and timely payout of pensions.

2. Benchmark Corpus

For each employee covered under NPS, who has exercised the UPS option, a benchmark corpus value shall be computed by CRA for comparison with individual corpus based on the following assumptions:

- (i) regular and timely receipt of applicable contributions of both, employer and employee, for each month of qualifying service.

- (ii) contributions being invested as per default pattern determined by the Authority;

- (iii) no partial withdrawals made during the accumulation phase;

- (iv) any voluntary contributions made shall not be considered; and

- (v) Any contributions for the period before the commencement of the qualifying service under the Central Government shall not be considered.

In UPS, the benchmark corpus is the amount you should have at retirement to secure the minimum guaranteed pension. If your NPS corpus is lower than the benchmark, you must deposit the shortfall amount from your savings, which can be a huge financial burden. You won’t receive the full pension as expected if you don’t meet the benchmark.

3. No Flexibility in Fund Withdrawals

Under NPS, you can withdraw a lump sum and use it as per your financial needs. In UPS, a majority of your corpus is locked into an annuity, leaving little for liquidity. Once you opt for UPS, you cannot opt back to NPS—it’s a one-time irreversible decision.

4. UPS Pension Is Lower for Short Service Employees

- The pension under UPS is directly linked to your last 12-month average Basic Pay.

- Since you are retiring after just 10 years of service, your pension will be significantly lower than those with 20-30 years of service.

- In contrast, under NPS, your corpus grows with market returns, potentially giving you a higher pension with additional investment options.

- In NPS even If you retire after 10 years you will get an equal amount of pension, assured by UPS. But, you may receive more lumpsum amounts in NPS than UPS. This is very important point to be considered to these employees who are thinking

- ups pension after 10 years

- ups pension after 15 years

5. No Market-Linked Growth Like NPS

- NPS investments grow based on market returns. Over 10+ years, this can significantly increase your retirement corpus.

- UPS doesn’t have market-linked returns—your pension is fixed and won’t increase over time except for DA revisions.

- Example: If markets perform well, NPS investors can receive double or even triple the returns compared to a fixed pension under UPS.

6. UPS Locks You Into Government Pension Dependency

- In UPS, your retirement income depends on government policies.

- Future policies might change pension structures, reducing benefits over time.

- In NPS, you have complete ownership of your funds, allowing you to invest in different retirement schemes.

- Haven’t you checked yet how much pension you receive right now if you quit job?

- Then you must try the official NPS pension calculator by NSDL.

- Also, compare your expected UPS pension using our UPS pension calculator.

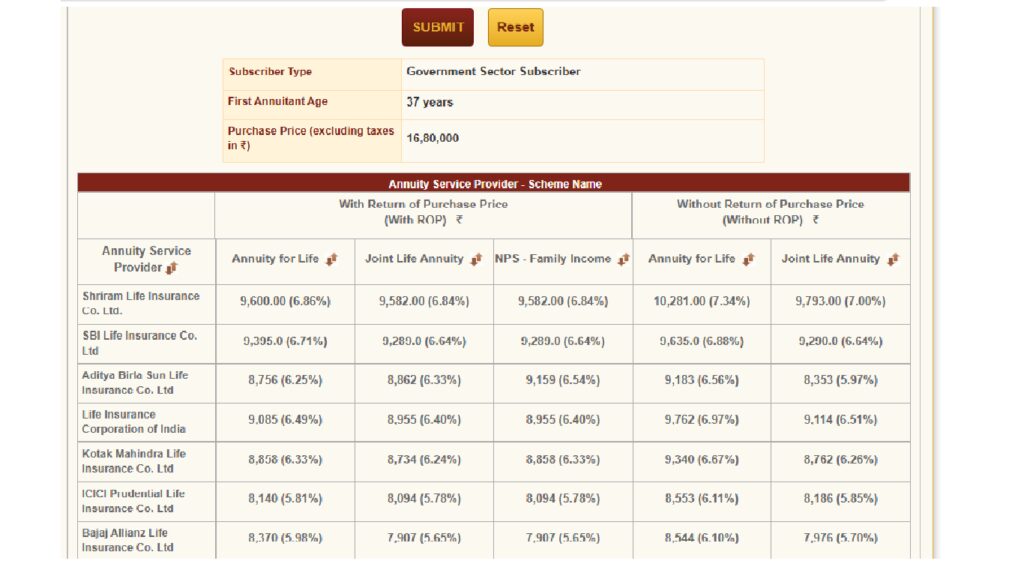

Example: Pension after 10 years of service NPS

A friend will complete 10 years in service with a projected NPS corpus of ₹21,00,000.

- 20% (₹4.2L) can be withdrawn

- 80% (₹16.8L) goes into annuity

This will give him a fixed monthly pension for life. Here is the screenshot of that friend’s pension using the above-suggested calculator.

I am sure that you understand UPS and NPS better now. Which one you choose, comment me below or if you need any suggestions you can freely ask me in the comment or email me your query.

Subscribe our newsletter to join with our financial freedom journey.

Frequently Asked Questions (FAQs)

How to change NPS to UPS?

It’s very simple you can apply to your Drawing and Distribution Officer (DDO), Or you can apply online using CRA official website.

Is UPS better than NPS?

It depends on your service period, retirement goals, and risk appetite:

UPS offers a fixed monthly pension after retirement, making it ideal for those who prefer stability and guaranteed income.

NPS offers market-linked returns, with flexibility and the potential for higher corpus, but it comes with investment risks.

📌 Important: Your decision should depend on the corpus, retirement age, and financial goals.

🔍 Read the full blog post to compare both schemes.

🔢 Use the official NPS Calculator and UPS Calculator on our website to make an informed choice.

How much Pension will I get from UPS?

Under UPS, you will receive 50% of your last 12 months average basic pay as a monthly pension. For example, if your average basic pay is ₹40,000, your UPS pension will be around ₹20,000 per month.

How do I get a 50000 pension per month?

To receive a ₹50,000 monthly pension under UPS, your last 12 months average basic pay should be ₹1,00,000, since UPS offers 50% of that as a pension.

What is the Unified Pension Scheme?

The Unified Pension Scheme (UPS) is a proposed alternative to the National Pension System (NPS) aimed at providing guaranteed monthly pensions to government employees after retirement.

Unlike NPS, which depends on market returns and corpus accumulation, UPS promises a fixed pension—usually 50% of the last drawn average basic pay—ensuring more stability and predictability for retirees.

What is the lump sum amount in UPS?

In the Unified Pension Scheme (UPS), there is no lump sum withdrawal like in NPS. Instead, If you have a surplus benchmark corpus in your account you will get the surplus amount as a lump sum withdrawal.

Example: At retirement time, you have 100000 as the last 12 months’ basic pay. You will receive 50000 as a guaranteed pension. For this, You must hold roughly 57,00,000 rupees as a benchmark corpus in your UPS or NPS account.

What is the Best Benchmark Corpus Calculator?

I got the approximate benchmark corpus value of 57 lakhs in the above answer using the UPS Pension Calculator. This gives you how much benchmark corpus you require at retirement. This also gives you how much surplus benchmark corpus you have or how much corpus you need to add more to get an assured UPS pension.